What is a Contra Entry in Housing Societies Accounting?

Maintaining accurate records is crucial for managing a society’s finances. In accounting, one special type of transaction that frequently comes up is the contra entry. In this blog, we’ll explore what a contra entry is, its significance in accounting, contra entry examples and step-by-step instructions on recording contra entries in your society’s accounting books, making your accounting and billing solutions easier.

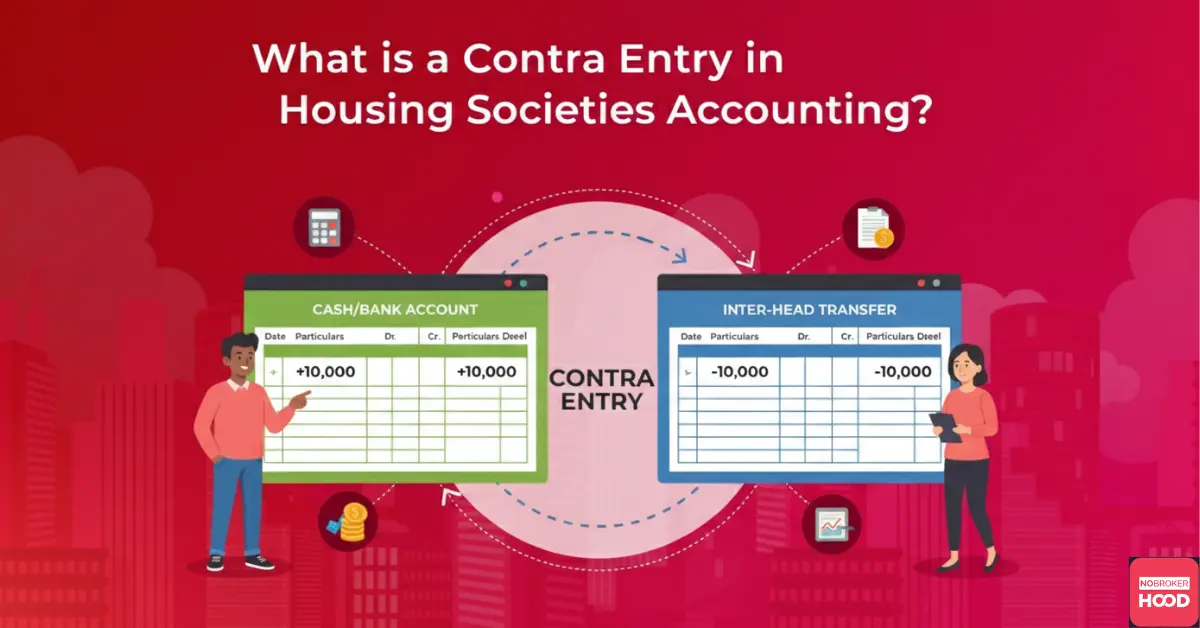

What is Contra Entry with Example?

A contra entry is an accounting transaction where funds are transferred between two similar accounts. This usually involves cash and bank accounts or transactions between two bank accounts. The key to understanding what a contra entry in accounting lies in its dual nature: it simultaneously debits and credits two related accounts without impacting the financial position of the society.

Contra Entry Example: Let’s say you transfer funds from the society’s main bank account to a petty cash account for minor expenses. Here, the cash account is debited, and the bank account is credited, but the total cash balance of the society remains the same.

Contra Entry Examples

To make contra entries easier to understand, let’s look at a few common contra entry examples:

1. Contra Entry for Cash Withdrawal for Petty Cash

If your society needs petty cash for daily expenses, you might withdraw cash from the bank. This results in a contra entry where the bank account is debited, and the cash account is credited.

2. Contra Entry for Cash Deposit into Bank

When you deposit cash into the bank, the cash account is debited, and the bank account is credited. This is a common contra entry for cash deposit.

3. Transfer Between Bank Accounts

If the society has multiple bank accounts, funds can be transferred between them. One bank account will be debited, while the other will be credited. This is known as a contra entry bank-to-bank transaction.

These contra entry examples illustrate what a contra entry example looks like, making it clear that contra entry in accounting involves transactions within similar accounts and often occurs when moving cash or funds between accounts.

Also Read: Effective Income and Expense Management for Gated Communities

Types of Contra Entry in Accounting

Contra entries in accounting are broadly classified based on the nature of the accounts involved:

Bank Account to Cash Account

When cash is withdrawn from the bank.

Cash Account to Bank Account

When cash is deposited into a bank account.

Bank Account to Bank Account

When transferring funds from one bank account to another.

Cash Account to Cash Account

In rare cases where two cash accounts exist, funds may be transferred between them.

In co-operative society accounting, these transactions typically arise when managing petty cash, making bank deposits, or balancing funds between accounts to meet daily expenses.

Benefits of Using a Contra Entry in Accounting

Contra entries streamline record-keeping by consolidating transactions involving cash and bank accounts into a single record. This helps keep your society’s financial books organised, ensuring accurate reporting and smooth reconciliation. Here’s what you mean by contra entry in a practical sense: it offsets transactions within accounts, simplifying financial tracking without affecting the society’s net cash position.

Contra Journal Entry in Accounting

A contra entry journal entry is recorded in the cash book. You’ll use two columns: one for cash and one for bank transactions. Contra entries are indicated with the letter “C” in the Ledger Folio (L.F.) column to denote that the transaction is internal.

Contra Account Journal Entry Examples

When a business withdraws cash from the bank for office use, the cash balance increases, and the bank balance decreases. This transaction is recorded as a contra entry because both accounts belong to the business.

Contra Entry Examples Table

| Transaction Type | Debit Account | Credit Account |

| Cash withdrawn from the bank | Cash Account | Bank Account |

| Cash deposited into the bank | Bank Account | Cash Account |

| Transfer from Bank A to Bank B | Receiving Bank | Paying Bank |

| Funds moved between cash accounts | Cash Account | Cash Account |

Journal Entry for Contra Entry

| Particulars | Debit (₹) | Credit (₹) |

| Cash A/c Dr | 10,000 | |

| To Bank A/c | 10,000 |

(Cash withdrawn from the bank for office use)

Contra Entry in Cash Book

| Date | Particulars | L.F. | Cash (Dr) | Bank (Cr) |

| Date | To Bank A/c | C | 10,000 | |

| Date | By Cash A/c | C | 10,000 |

Read also: Choosing the Right Accountant for Your Apartment Society

Step-by-Step Guide for Recording Contra Entry in Cash Book

To correctly record a contra entry in cash book, follow these steps:

Identify the Accounts Involved

Contra entries only apply to cash and bank accounts. Before recording, ensure that the transaction is between these accounts.

Determine Debit and Credit Entries

Decide which account will be debited and which will be credited. For example, if you are depositing cash into the bank, debit the cash account and credit the bank account.

Record in the Cash Book

Enter the details on the debit side for the receiving account and on the credit side for the giving account.

Mark as Contra

Label each entry as a contra by writing “C” in the L.F. column to indicate that the transaction does not impact the society’s financial position.

Double-Check Entries

Verify that each debit entry has a corresponding credit entry and that all details match the actual transaction.

Read also: Choosing the Right Accountant for Your Apartment Society

Advantages of Contra Entries

Using contra entries offers several benefits:

Efficient Record-Keeping

Contra entries make it easier to record internal transactions involving cash and bank accounts, providing a consolidated view.

Accurate Financial Reporting

These entries ensure that all cash and bank transactions are accurately tracked and reported.

Simplified Reconciliation

Since contra entries offset each other, they simplify the process of balancing cash and bank accounts at the end of the month.

Disadvantages of Contra Entries

While contra entries offer many advantages, there are some downsides to consider:

Increased Complexity

Each transaction requires both a debit and a credit entry, which can be confusing if not done correctly.

Potential for Errors

Mistakes can happen if a bookkeeper misinterprets what a contra entry is in accounting, leading to inaccuracies in the financial books.

Limited Scope

Contra entries are specific to cash and bank accounts and don’t apply to other types of transactions.

How NoBrokerHood Helps in Accounting Management for Housing Societies

NoBrokerHood simplifies accounting management by acting as an all-in-one society accounting app. It automates billing, tracks expenses, manages payments, and generates accurate financial reports, helping housing societies maintain transparent, error-free, and efficient accounting systems.

| Feature | How NoBrokerHood Helps |

| Society Accounting App | NoBrokerHood works as a complete society accounting app to manage day-to-day financial activities. |

| Automated Billing | Automatically generates maintenance bills and tracks dues from members. |

| Expense Tracking | Records all society expenses such as utilities, repairs, and vendor payments in one place. |

| Online Payment Integration | Allows residents to pay maintenance online, reducing manual entry errors. |

| Ledger Management | Maintains member-wise and vendor-wise ledgers for transparent accounting. |

| Reports & Statements | Generates income–expense reports, balance sheets, and audit-ready statements. |

| Bank Reconciliation | Simplifies matching bank transactions with society records. |

| Compliance Support | Helps societies stay organised for audits and statutory requirements. |

All Solutions by NoBrokerHood:

Summary

Understanding and recording contra entries in your society’s accounting books is essential for accurate bookkeeping. Contra entries help manage cash flows between bank and cash accounts while keeping financial statements organised. By following the steps and format outlined above, societies can ensure they’re handling contra entries correctly, leading to accurate financial records and smoother reconciliation.

FAQs

A contra entry is an accounting entry that involves a transfer of funds between cash and bank accounts or between two bank accounts, where one account is debited, and the other is credited.

For a cash withdrawal from the bank, you should debit the cash account and credit the bank account in your cash book, marking it with “C” for contra.

Contra entries are crucial for accurate record-keeping, especially for tracking transfers between cash and bank accounts. They help streamline financial reporting and simplify reconciliation.

An example of a contra entry is when cash is deposited into a bank account. Here, the cash account is debited, and the bank account is credited.

No, contra entries do not affect the overall financial position, as they simply transfer funds within similar accounts (cash or bank) without changing the net cash position of the society.