Cooperative Society Accounting: Issues & Best Practices

In India, cooperative societies need to keep clear financial records according to the Societies Registration Act 1860. Many societies find this challenging, and it can sometimes lead to misunderstandings between the residents and the management board. Switching from manual bookkeeping to digital accounting will make managing finances easier and transparent.

By regular monitoring and the usage of cashless payments, societies can stay organised and meet obligations like TDS and GST without stress. Digital tools help committees manage accounts efficiently while keeping everything accountable and clear.

Common Accounting Issues Faced by Cooperative Societies

The nature of accounting records required by cooperative societies is notably different from traditional businesses.

The main issues facing societies from an accounting standpoint include:

- Classifying a member’s shares as equity or liability

- Revenue recognition, there can be multiple performance obligations involved

- Difficult financial record-keeping while complying with principles of cooperation and compliance obligations

It is not uncommon for societies to also experience weaknesses in internal controls. These can include internal control weaknesses using the framework established by the Committee of Sponsoring Organisations of the Treadway Commission, which focuses on financial reporting risk.

Some common internal control weaknesses are:

- No adequate segregation of duties,

- The transaction records provided by a member are not complete,

- Delays in financial reporting,

- Complex requirements for statutory compliance.

There is a lack of cohesiveness at the state and national levels associated with the accounting systems that apply to cooperative accounting.

- Current accounting standards are not consistent with cooperative values and principles.

- It is difficult to demonstrate the socio-economic contributions made with cooperative financial statements.

Financial constraints:

Many cooperatives are unable to raise capital to employ trained accountants and to maintain and safeguard records. This impacts the financial management of the society.

How to Maintain Society Accounts

Keeping society’s accounts is not that complicated when the accounts are well-managed. The audits become easier, disputes are minimised, and members feel confident in the committee’s handling of funds. Here’s a practical guide on how to maintain society accounts effectively:

Maintain a Standard Chart of Accounts

Set up a clear and consistent chart of accounts for income, repair fund, staff salaries, utility bills and bank charges. This setup will simplify bookkeeping and will simplify audits. This will help you to quickly locate any transaction.

Record Transactions Every Day

Record maintenance charges, utility bills, salaries, repairs, and vendor payments every day. Do not let it pile up. Daily updates will reduce errors and keep the society’s finances clear.

Follow the Double-Entry System

Every transaction should have a matching debit and credit entry. This will reduce mistakes and provide a clear picture of the society’s financial health.

Dedicated Society Accounting Software

A Society accounting software can maintain bills, receipts, ledgers, TDS deductions, and GST compliance. It keeps your accounts ready for audits by reducing manual work and errors.

Reconcile Bank Statements Monthly

Cross-check your bank statements with your books every month. This will spot missing entries, unrecorded cheques, pending deposits, or bank charges before they become serious issues.

Keep a Separate Bank Account for the Society

Never mix personal and society funds. A dedicated account ensures cleaner financial records and makes audits faster and simpler. It will also build trust and reflect transparency.

Prepare Monthly Financial Statements

Generate an Income & Expenditure Statement, Balance Sheet, and Cash Flow Statement every month. These reports will help the committee track budgets, make informed decisions, and spot any financial trends early.

Keep Records for 7 to 10 Years

The cooperative laws state that the Society’s financial documents should be recorded for at least 7 to 10 years. Proper documentation is essential for audits, legal compliance, and resolving any disputes.

Conduct Annual Audits Promptly

Audits should be completed within 60 days of the financial year-end. During this process, auditors check cash balances, legal compliance, pending dues, and maintenance collections to ensure all accounts are accurate and up to date.

Read also: How to Prepare Final Accounts of Cooperative Society

Essential Documents for Cooperative Society Accounting

To keep society’s finances transparent and well-organised, it’s important to maintain proper records of all transactions. Essential documents include:

- Member Contribution Records, including membership fees, share capital, and maintenance payments from members.

- Receipts and Invoices of all expenses, like repairs, utility bills, and vendor payments.

- Salaries, deductions, and benefits of the staff.

- Monthly statements for all society accounts that have to be reconciled with transactions in future.

- Document any investments, loans, or borrowings.

- Tax Documents including TDS, GST challans, returns, and other statutory filings.

- The past audit Reports will help for reference and compliance checks.

- Other Supporting Documents – Store agreements, legal papers, or receipts related to society finances.

- Properly maintaining these documents ensures smooth audits, boosts transparency, helps settle disputes, and keeps society compliant with legal requirements.

Tips for Cooperative Society Accounting

- Keep records: Maintain clear financial records for 7 years.

- Separate duties: Divide authorisation, custody, and recording tasks.

- Reconcile regularly: Check accounts and balances monthly.

- Internal controls: Secure assets, cash, and documents.

- Review finances: Track income, expenses, and cash flow.

- Tax compliance: File TDS, GST, and maintain documents.

- Use software: Adopt easy-to-use accounting tools.

- Go digital: Minimise cash; use banking apps and UPI.

Also Read:Choosing the Right Accountant for Your Apartment Society: What to look for

Annual Financial Management Processes

Annual financial management processes are essential for proper financial management of societies. The key activities include:

- Preparation of monthly trial balances and monthly adjustments

- Preparation and submission of audit reports within six months of the year’s end

- Retention of accounting records for a minimum of ten years

The annual audit, which must be performed within 60 days after a financial year-end, reconciles at a minimum the cash balances, securities, and debts overdue. The board members must also ensure adequate internal controls and appropriate management of financial and accounting records during the full fiscal year! Audited financial statements should be circulated and reviewed at the Annual General Meeting (AGM) within the six-month time limit allowed after the financial year-end.

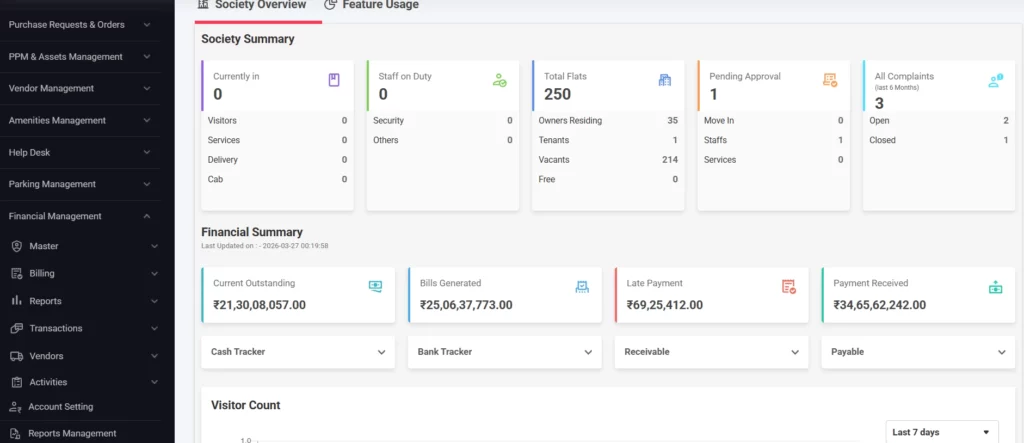

Society Accounting System by NoBrokerHood

NoBrokerHood’s society accounting software has been designed specifically to solve the financial problems facing cooperative housing societies. It is an end-to-end solution that simplifies record-keeping, compliance, and transparency. Automated billing and real-time expense tracking, along with digital ledger/workbook management, eliminate manual work and human errors.

Treasurers and management committees can generate reports, deal with member contributions, and file TDS and GST more easily. The software supports cashless transactions through UPI and bank integrations, facilitating a move towards digital-first, audit-ready, cooperative accounting. NoBrokerHood plays a major role in maintaining the society’s financial records accurately.

All Solutions by NoBrokerHood:

FAQ’s

Q1. What are the basic accounting rules for cooperative societies?

Cooperative societies typically maintain double-entry bookkeeping systems, and all transactions must be recorded in a daybook for transparency.

Q2. How should a cooperative society manage its financial records on an annual basis?

Hold budget meetings, prepare monthly trial balances, submit audit reports within 60 days of year-end, and retain records for 10 years.

Q3. What are the best practices for accounting for an effective cooperative housing society?

Maintain accurate records, segregate duties, implement and review internal controls, resolve tax issues, and use up-to-date society-specific accounting software.

Q4. How can cooperative societies reduce cash transactions?

Use digital payments, plan cash budgets, maintain bank accounts, and implement effective cash management.

Q5. What financial statements are needed for a cooperative society?

The Balance Sheet or Financial Statement reports the year-end financial position and accounting results.